![]()

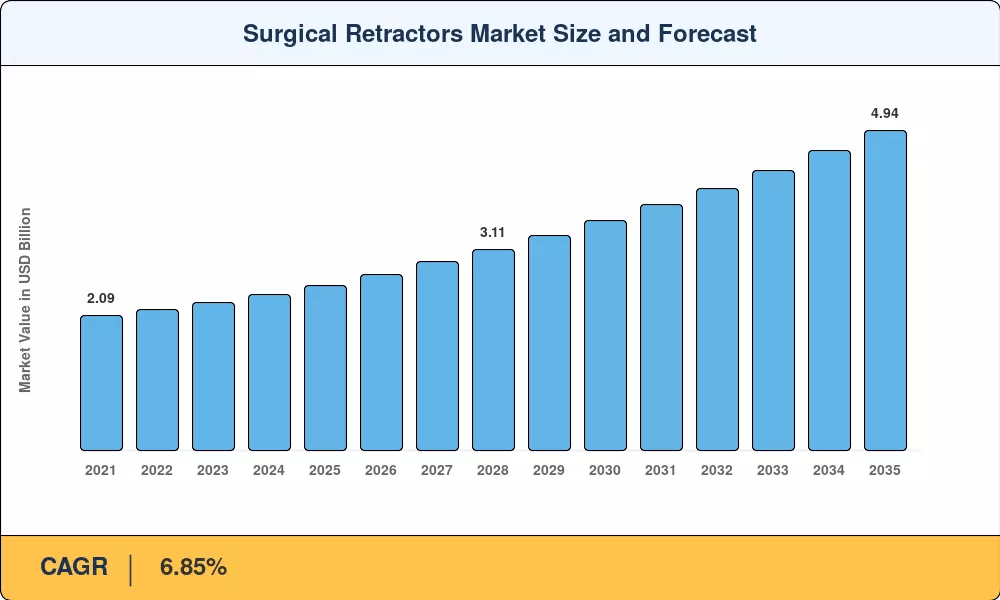

Surgical Retractors Market to Expand from USD 2.72 Billion in 2026 to USD 4.94 Billion by 2035—Driven by Post-Pandemic Surgical Volume Recovery

NY, CA, UNITED STATES, June 24, 2026 /EINPresswire.com/ — As per Market Research Future, the global Surgical Retractors Market size is projected to reach USD 4.94 Billion by 2035 from USD 2.72 Billion in 2026, at a CAGR of 6.85% during the forecast period 2026–2035. The market base was estimated at USD 2.55 Billion in 2025.

The 6.85% CAGR—anchored by structural procedural volume growth rather than discretionary healthcare spending—is driven by three converging forces: post-pandemic surgical volume recovery that has cleared backlogs in deferred orthopedic and cardiovascular procedures, sustained LED-illuminated and polymer-framed instrument innovation that is replacing legacy stainless-steel hand-held retractors with lighter, navigation-compatible alternatives, and the global expansion of ambulatory surgery centers that is converting inpatient procedural demand into high-throughput outpatient retraction-device utilization.

National governments and multilateral health organizations are amplifying this momentum. The US Hospital Infrastructure Reinvestment Act (2024) catalyzed hospital capital-equipment refresh cycles, directly addressing aging instrument fleets that constrained operating-room efficiency. Smart OR instrumentation received more than USD 1.8 billion in global medtech venture funding in 2024, and the transition to the EU Medical Device Regulation (MDR 2017/745) is accelerating uptake of single-use sterile variations.

Request A Free Sample:

https://www.marketresearchfuture.com/sample_request/7019

Key Market Trends & Growth Drivers

Post-Pandemic Surgical Volume Recovery and Deferred Procedure Clearance

Post-pandemic surgical volume recovery—particularly in deferred orthopedic and cardiovascular procedures—has created a structural demand surge that extends beyond simple backlog clearance. The WHO Global Status Report on Road Safety 2024 records that approximately 1.35 million people die in traffic accidents annually, with 20 to 50 million more suffering non-fatal injuries, many requiring surgical intervention. Because orthopedic and trauma procedures are among the most retractor-intensive surgeries, this injury burden mechanically expands the addressable population for surgical retractor utilization.

National surgical plans in Ethiopia, Rwanda, and Bangladesh are building district-level operating capacity, feeding into the Surgical Retractors Market growth pipeline across emerging economies. Each percentage point of surgical volume gain translates into measurable instrument procurement, and the embedded retraction-device replacement schedule in routine surgical care makes this driver structurally durable through 2035.

LED-Illuminated and Polymer-Framed Instrument Innovation

Legacy stainless-steel hand-held retractors, long the default instrument modality, are giving ground to LED-illuminated, polymer-framed devices that lower instrument weight by as much as 40% and integrate with surgical navigation platforms. Self-retaining systems captured approximately 57% of the Surgical Retractors Market in 2025, reflecting surgeon preference for hands-free tissue exposure in complex procedures.

The Bookwalter, Thompson, and Omni-Tract systems remain institutional standards, though next-generation polymer-framed variants are gaining traction for weight reduction and MRI compatibility. The US Hospital Infrastructure Reinvestment Act (2024) committed federal funding to hospital capital-equipment refresh cycles, directly addressing aging instrument fleets that constrained operating-room efficiency.

Ambulatory Surgery Center Expansion and Outpatient Shift

The global expansion of ambulatory surgery centers—accelerated by payer incentives favoring same-day discharge—ties provider reimbursement to throughput and efficiency metrics. Data from the Ambulatory Surgery Center Association show that ASCs perform over 60% of all outpatient surgical procedures in the United States, with average case volumes growing 8–10% annually.

This economic incentive has driven hospital formulary committees to prioritize disposable and single-use retractor variants, shifting procurement budgets toward the Surgical Retractors Market at the expense of capital-intensive reusable set spending. Value-based surgical contracts in the United States and European reference pricing for instrument trays have shifted institutional procurement toward leaner, procedure-specific configurations.

Ask for Customization:

https://www.marketresearchfuture.com/ask_for_customize/7019

Market Segment Insights

BY PRODUCT TYPE

Self-Retaining Retractors: Dominant segment with ~57% revenue share in 2025. Reflecting entrenched surgeon preference for hands-free tissue exposure in multi-hour procedures across abdominal, thoracic, and orthopedic specialties. The Bookwalter, Thompson, and Omni-Tract systems anchor institutional formularies globally due to their reliability and decades of clinical evidence supporting self-retaining exposure. Hospital procurement teams treat them as default standards in complex procedures, and established pricing has enabled broad adoption even in cost-sensitive emerging markets.

Illuminated/Fiber-Optic Retractors: Fastest-growing product segment at 8.22% CAGR (2026–2035). Driven by new LED-integrated approvals and expanding deep-cavity visualization indications. LED-integrated blade systems from Medtronic and Teleflex generated over USD 0.31 billion in 2025 revenue, and pipeline wireless-enabled variants targeting neurosurgical and spinal procedures could double the segment’s addressable population by 2030. The convergence of illumination technology with self-retaining frames is creating integrated platforms that personalize surgical exposure at scale.

BY APPLICATION

General Surgery: Dominant application with ~48.6% revenue share in 2025. High volume of abdominal procedures such as laparotomies, hernia repairs, and gastrointestinal surgeries makes general surgical retraction a near-universal component of the operative care pathway. The inherent procedural diversity of general surgery drives sustained dual-channel demand for both hand-held and self-retaining instruments.

Neurosurgery: Fastest-growing application segment at 8.5% CAGR (2026–2035). Reflecting improved visualization requirements that extend the window for illuminated retractor utilization. Complex cranial and spinal procedures create a larger prevalent population requiring sustained precision retraction.

BY MATERIAL

Stainless Steel: Dominant material with ~60% revenue share in 2025. Durability and established sterilization workflows anchor institutional procurement. Stainless steel sets from B. Braun and Integra LifeSciences remain the default in high-sterilization-cycle environments, with hospital procurement teams treating them as capital assets with 7–10 year replacement cycles.

High-Performance Polymers: Fastest-growing material segment at 10.22% CAGR (2026–2035). Lightweight alternatives and MRI compatibility drive demand. Polymer-framed variants reduce instrument weight by up to 40% and integrate with surgical navigation platforms, enabling cancer bone spread treatment in community clinics lacking specialized infrastructure.

BY END USER

Hospitals: Largest segment with ~52% share in 2025. Comprehensive surgical service lines and complex procedure requirements dominate volume. Hospitals remain the primary delivery site for self-retaining and table-mounted systems due to capital-equipment budgets, specialized sterile processing, and surgeon training infrastructure.

Ambulatory Surgical Centers: Fastest-growing end-user segment at 10.5% CAGR (2026–2035). Outpatient shift and cost optimization drive demand as disposable and single-use retractors reduce the need for central sterile processing. ASCs and community surgical clinics increasingly prescribe disposable retractor options to manage reprocessing capacity and infection-control liability.

Read Detailed Insights:

https://www.marketresearchfuture.com/reports/surgical-retractors-market-7019

Regional Outlook

North America — Dominant Market (~42.0% Share, 2025)

The United States generates approximately 78% of North American Surgical Retractors Market revenue, driven by the Hospital Infrastructure Reinvestment Act (2024) capital-equipment refresh cycles, commercial insurance coverage of premium illuminated retractors as standard-of-care, and broad reimbursement for self-retaining system regimens—a single policy ecosystem that converted a capital-constrained market into one with a structural preventive instrument tail.

CMS reimbursement for outpatient surgical procedures under the hospital outpatient prospective payment system has driven adoption in academic medical centers, while community surgery networks increasingly prescribe disposable retractor options to manage sterile-processing capacity. The US dominates through a combination of high per-procedure spending, robust payer coverage, and rapid illuminated-retractor adoption.

Europe — Second Largest (USD 0.70 Billion, 2025)

Europe’s Surgical Retractors Market reflects divergent national strategies—Germany leads regionally with AMNOG rapid assessment of new instrument technologies, contributing USD 0.18 Billion in 2025, while the UK historically used selective retractor targeting before broadening coverage through NICE technology appraisals for illuminated systems at 6.8% CAGR.

France contributes ~18.5% of regional share through early-access programs for polymer-framed retractors. Italy contributes USD 0.09 Billion on AIFA reimbursement for single-use instrument sets. Spain is growing at 6.4% CAGR on National Health System investment.

Asia-Pacific — Fastest-Growing Region (9.58% CAGR, 2026–2035)

Asia-Pacific is the engine of the Surgical Retractors Market. China holds the largest regional share with ~34.8% of regional revenue, driven by greenfield hospital investments and the 2024 expansion of outpatient surgical coverage under the National Healthcare Security Administration—instantly extending retractor demand to over 1.3 billion insured lives.

India is growing at 11.2% CAGR on the back of Ayushman Bharat surgical package expansion. Japan contributes USD 0.22 Billion through NHI pricing for next-generation illuminated systems at steady pace. South Korea is growing at 9.8% CAGR on HIRA surgical reimbursement reform.

Middle East & Africa — Emerging Opportunity (6.0% Share, 2025)

The Middle East & Africa is bifurcated between well-funded Gulf states and resource-constrained Sub-Saharan nations. Saudi Arabia leads the region with Vision 2030 healthcare cluster development, contributing ~32% of regional share—NEOM health cluster and the UAE’s Cleveland Clinic and Mayo Clinic affiliations have created pockets of excellence for advanced surgical instrumentation. The UAE is growing at 8.5% CAGR on medical tourism for complex procedures. South Africa contributes USD 0.04 Billion on National Health Insurance surgical inclusion.

South America — Growing Presence (USD 0.17 Billion, 2025)

Brazil anchors South America’s Surgical Retractors Market at ~58.4% of regional revenue, with the Unified Health System (SUS) incorporating standardized instrument trays into the national surgical protocol in 2023, providing a stable demand floor that smooths regional forecasts.

Access to premium illuminated retractors remains limited by import dependencies, though the Brazilian Ministry of Health has initiated domestic polymer-framed instrument production feasibility studies. Argentina is growing at 7.8% CAGR on private surgical clinic expansion.

Competitive Landscape and Recent Developments

The Surgical Retractors Market displays medium concentration, with the top five companies holding an estimated 45–52% combined revenue share. The Herfindahl-Hirschman Index sits in the 900–1,400 range, reflecting a mix of multinational medical device leaders and specialized surgical instrument developers. Patent expirations and generic instrument entry are gradually fragmenting branded segments, though pipeline innovation in illuminated and smart retractor systems sustains competitive moats for first-movers.

The competitive landscape is stratified between self-retaining system pioneers serving global surgical markets, illumination-technology specialists capturing premium tenders, and disposable instrument developers consolidating the infection-control segment.

KEY COMPANIES AND RECENT MILESTONES

Medtronic (2024–2025): Maintains leadership with the Touch Surgery ecosystem and integrated OR platform, commanding ~12–16% of global Surgical Retractors Market revenue. First-mover in smart OR instrumentation with global surgical workflow leadership. Premium platform positioning in academic medical centers offsets price compression in competitive markets.

Johnson & Johnson / Ethicon (2024–2025): Ottava surgical robotics platform and self-retaining instrument portfolio reinforce the integrated procedural solutions positioning, holding ~10–14% of global revenue. The company benefits from the structural bundle-contract tail created by expanded value-based surgical agreements.

Stryker (2024–2025): Orthopedic and neurosurgical retractor systems reinforce the specialty-specific instrumentation positioning, holding ~8–11% of global revenue. The Mako SmartRobotics ecosystem creates pull-through demand for compatible retractor sets in joint-replacement procedures.

Braun Melsungen AG (2024–2025): Aesculap instrument portfolio and high-volume stainless-steel production reinforce the cost-optimized, high-durability positioning, holding ~6–9% of global revenue. European MDR compliance expertise sustains market access advantages.

Integra LifeSciences (2024–2025): Neurosurgical and wound-retraction specialization reinforces the precision-surgery positioning, holding ~4–7% of global revenue.

Future Outlook: 2026–2035

By 2030, smart retractor systems with integrated sensors and AI-driven workflow optimization will become the operating system of surgical exposure management. The convergence of illumination technology, polymer materials, and digital integration will reshape the Surgical Retractors Market through the late 2020s. By 2030, an estimated 35% of newly installed self-retaining systems in academic medical centers will feature integrated LED illumination and navigation compatibility, creating a hardware-software revenue loop.

The US Hospital Infrastructure Reinvestment Act ensures domestic capital-equipment refresh cycles scale alongside procedural demand. Machine-learning models that integrate surgical workflow, instrument utilization, and outcome data can recommend optimal retractor selection and tray configuration for individual procedures. Start-ups have raised over USD 800 million in venture funding for surgical decision-support tools since 2023.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/surgical-equipment-market-556

https://www.marketresearchfuture.com/reports/minimally-invasive-surgery-devices-market-7875

https://www.marketresearchfuture.com/reports/surgical-robots-market-3025

https://www.marketresearchfuture.com/reports/operating-room-equipment-supplies-market-12510

https://www.marketresearchfuture.com/reports/orthopedic-devices-market-3323

https://www.marketresearchfuture.com/reports/neurology-devices-market-9768

https://www.marketresearchfuture.com/reports/laparoscopy-device-market-6312

https://www.marketresearchfuture.com/reports/surgical-navigation-systems-market-7863

https://www.marketresearchfuture.com/reports/wound-closure-devices-market-2001

https://www.marketresearchfuture.com/reports/general-surgical-devices-market-5864

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery